The fall market has officially come to an end and what a year it’s been on so many levels!

Typically the fall market runs from the second week of September until mid December. Last year I recall working a busy December market right up until the third week of December. Despite a handful of impressive sales over the past few weeks that attracted double-digit multiple offers, it has felt that the fall market ended a couple of weeks ago.

New quality listings continue to be very scarce leaving all of my buyers with limited to no options. It’s been a frustrating fall market to say the least.

As a friendly reminder, I mentioned last month that I had started to see some early signs of increased activity over the last week of October and first week of November and that this Fall market feels eerily similar to 2021.

This has continued on throughout November, though please note it’s a very small sample size.

While it’s clearly impossible to predict the future of the market, I do suspect that pent up buyer demand could drive a busier Spring Market in some segments of the GTA if quality listings finally hit MLS.

Inventory can’t really get any worse so I’m optimistic that more options will present in 2023 LOL.

November TRREB Stats

I feel like I’m beating a dead horse by saying this again, but November was another historically slow month (as far as November’s go). I wish I had something more exciting to share…

I’ve seen a lot of articles since the TRREB stats came out this week about sale prices dropping again, but I actually pointed out that this was basically a guarantee as it is a typical part of the annual cycle. It shouldn’t be a surprise. The market is slow and in a holding pattern, and news outlets are just looking for something to write about. The truth is, there isn’t much going on!

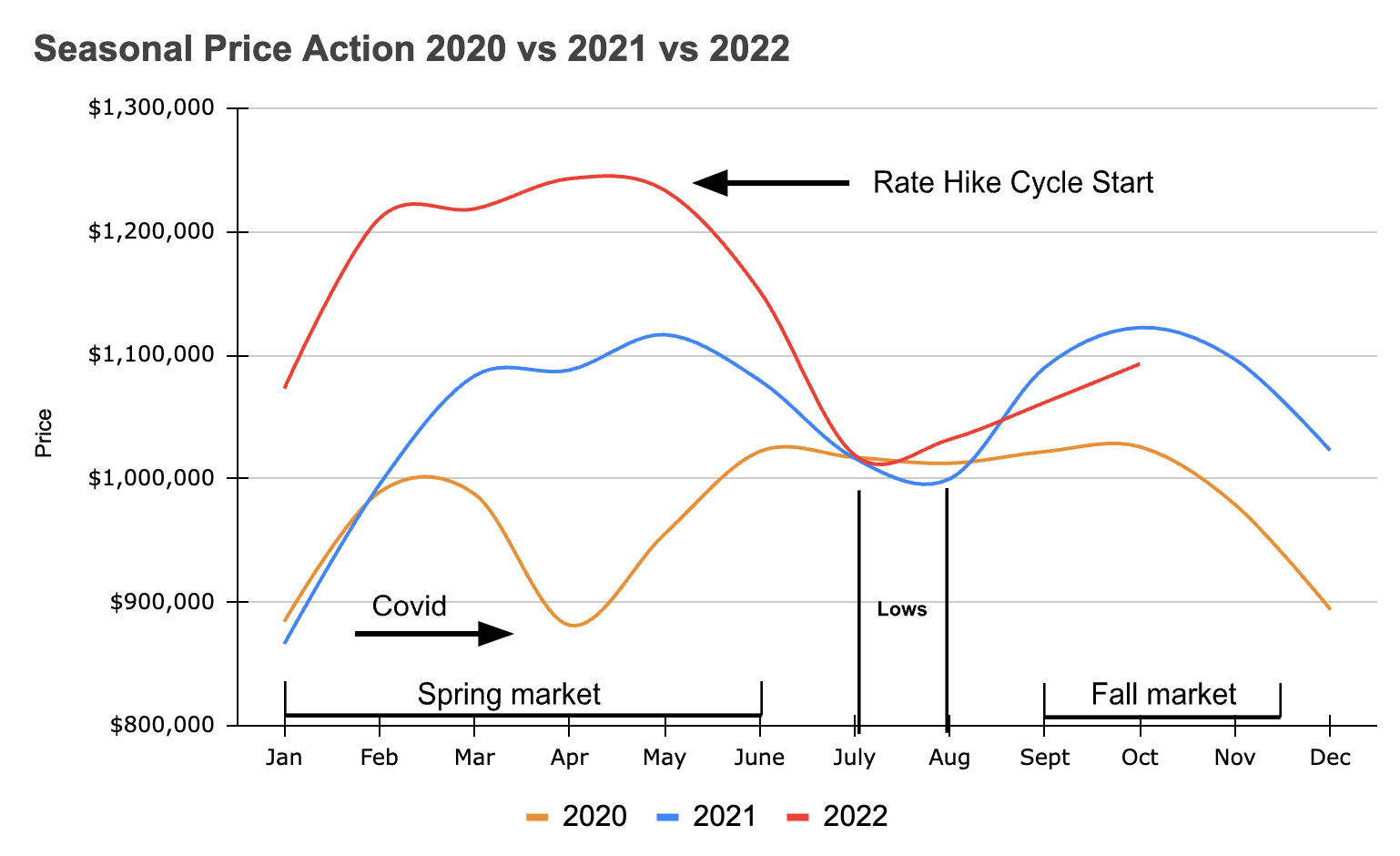

In my last report I shared this graph of the trajectory of sale prices as of October 2022 (red line), and comparing that to 2020 and 2021👇

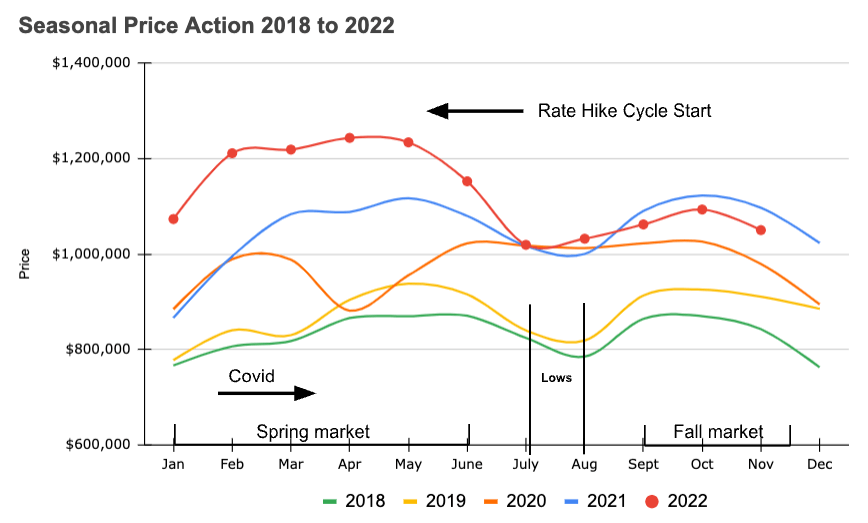

You can see that in 2020 and 2021 we had a drop in average sale price right around this time. So why would this year be any different when interest rates are much higher? Here is the same graph including the latest numbers from November.

As expected, reported average sale prices are headed downwards. I added in trend lines for 2018 & 2019 as well to show this isn’t just a pandemic anomaly–it’s cyclical.

In my opinion, stats don’t always do a good job of telling the story of what is actually happening on the ground. We’re dealing with averages spread over large area’s with varying microeconomic conditions.

What I’m seeing on the ground is that accurately priced, quality properties are still moving quickly, their typically receiving more than 1 offer, and are achieving above average sale prices.

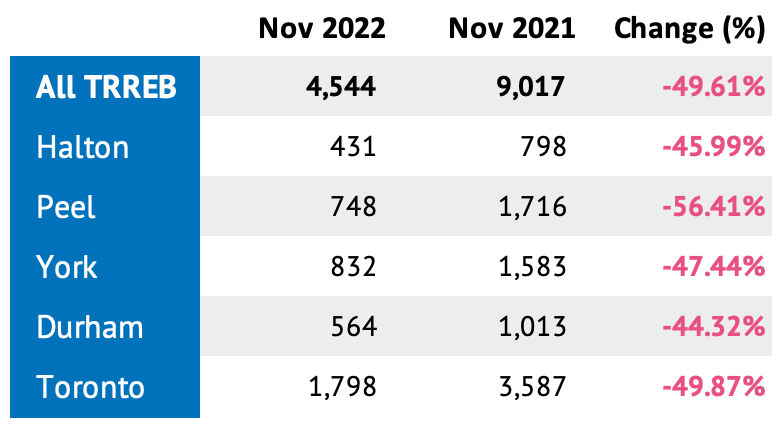

Number of Sales Year-over-year

We usually don’t see a slowdown in activity until the end of November, but the fall market ended prematurely this year with an almost 50% drop in sales activity.

Average Sale Price Year-over-year

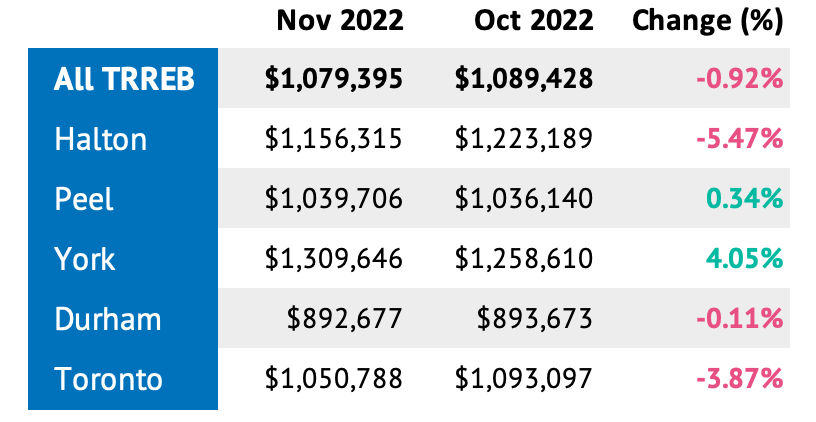

Average Sale Price Month-over-month

Prices are down as expected, but they can’t really tell us much about where we’re going in 2023.

If you look back up at those graphs, by November-December the average sale price almost always reverts to where it was around June-July of the same year.

Now that the fall market is behind us, and we have the full years worth of data, we can see that most of the damage was done by the summer, and we have hit a bit of a holding pattern in the market.

Looking to 2023

The data for December has almost no impact on what to expect in January and February, and while my on the ground insights have helped me prepare for Spring Markets in the past, there have been too few sales to really gauge what is in store for 2023, so I likely won’t discuss December’s TRREB stats next month unless something crazy happens. The market mostly shuts down for the holidays.

January/February activity is generally what sets that stage for the rest of the year. I would be shocked if a good listing, that is priced accurately, didn’t get all the love in January, despite where interest rates are at. I can feel and see buyer demand building with each lackluster month that has passed this fall.

There are some indications in the Bank of Canada’s press release comments that they may hold here for a cycle, but we’ll see on January 26th if that’s true, and if it is, what it does to the market.

If we don’t get a chance to talk before the holidays, hope you enjoy some delicious food, laughs, and have a Happy New Year!

(If you have questions, need advice, or want to talk about what I’m seeing out there, get in touch).