Momentum in the spring market continued building in April with sale prices, and sales activity picked up more steam from March. Supply is still very tight and was the main driver behind a 6% average sale price increase in Toronto.

Key Developments

- Inventory is still very low

- Bank of Canada (BoC) policy interest rate remains at 4.5%

- Next Bank of Canada interest rate meeting isn’t until June 7th

- CPI inflation rose to 4.4% in April from 4.3% in March

Aimee’s Experience

The only word I have to describe what is going on over the last few weeks in the market is “weirdness”. Especially when it comes to some offer nights I’ve competed in, or watched from the sidelines.

From a complete gut job semi in Central Toronto that got 16 offers and went for as much as it was probably worth at the peak of the market in 2022, to another really cute-as-a-button semi in the East End that got no love and went for 5% lower than the Seller’s purchased it in 2021.

Most properties are going for right around what I thought they would, but there are outliers like these that make the market feel a bit spotty. Prices have been steadily on the rise, but it seems like there is still a tug-of-war going on between the bears and the bulls depending on the home.

Sellers with homes worth below the $1.5M price range are mostly choosing to list under market value, hold back on offers, and have an offer night. This typically indicates a stronger seller’s market since you need demand to outweigh supply for it to work well.

I’ll tell you from my experience at this price point, especially for Freeholds (detached, semi, townhouse) it’s very competitive and is definitely in the seller’s favour right now.

At the higher price points, there is a 50/50 mix of listing strategies. There are still a lot of homeowners choosing to list at or slightly above fair market value and accepting offers any time. It feels a little more balanced on this side of the market. A lot more one-on-one negotiation between the buyer and seller to come to a deal.

April TRREB Stats

I really expected to see more inventory at this point based on seasonal norms and how strong the demand is. It just hasn’t happened. In the previous two years, the market leveled out/dipped in May and June because of an increase in inventory, but I don’t see any signs of that happening so far and it’s driving up prices.

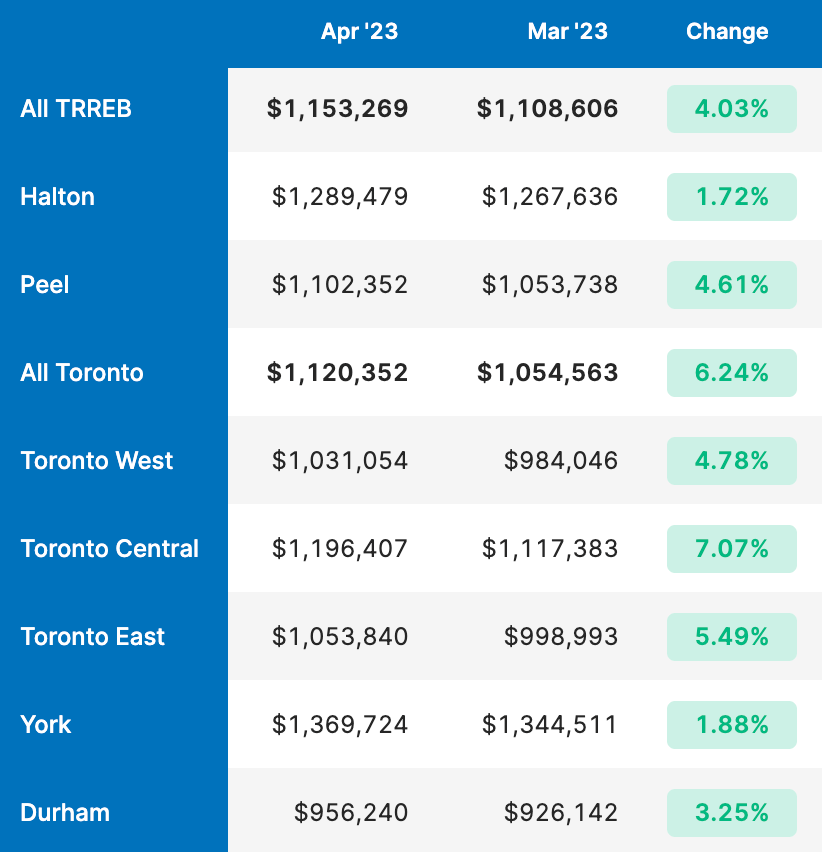

Average Sale Prices

Average sale prices across TRREB are up ~4%. This was mainly driven by Toronto (+6.24%) and Peel (+4.61%) but prices were up across all TRREB regions. We haven’t seen a month-over-month increase like this since early 2022. It’s more confirmation that the bottom has come and gone (barring some unforeseen event).

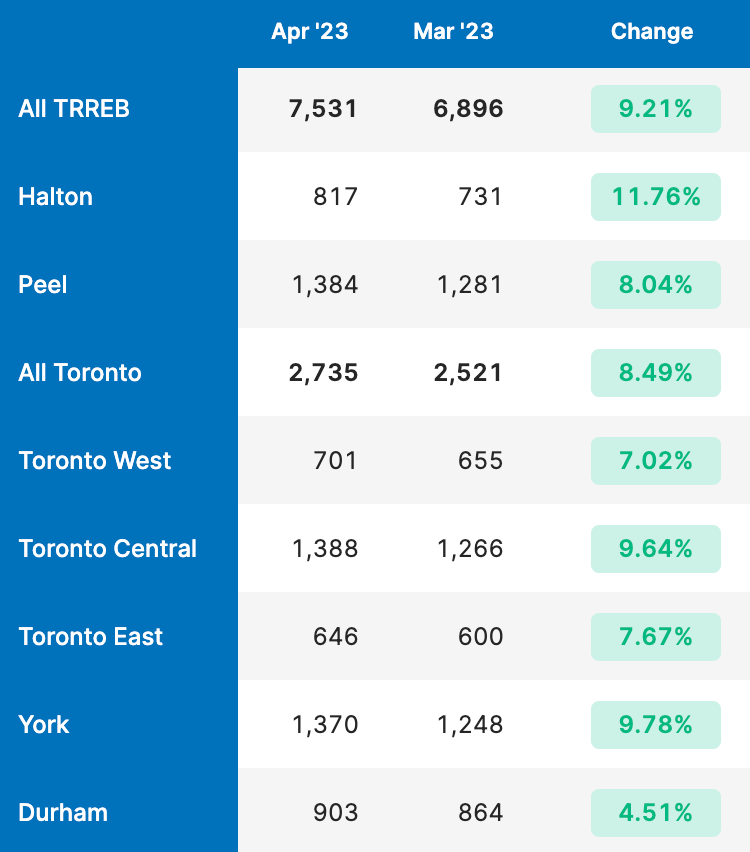

Sales and New Listings

Sales are up about ~9% from March 2023 (see table below), which is consistent with past years as we get more into the meat of the Spring market, sales activity picks up.

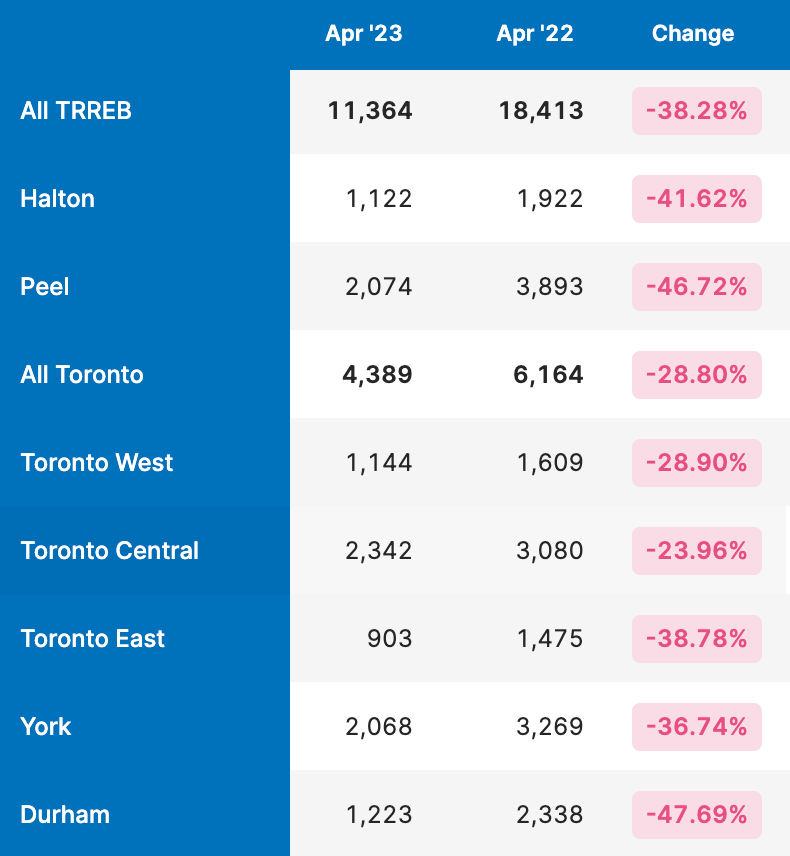

Year-over-year sales are only down slightly from April 2022 by ~6% (see table below) and ~10% in Toronto.

When you look at the fact that year-over-year sales only decreased slightly, and compare that with New Listings year-over-year (see table below), the supply issue becomes glaringly obvious.

Almost 40% less new inventory this April compared to 2022 (about 7,000 fewer listings), but only a slight dip in sales. That tells us that demand heavily outweighs supply. It’s probably even worse than what the data shows because I would argue that buyer sentiment is stronger today than last April when we were in the middle of the market correction.

Final Thoughts

If we don’t see more listings hit the market, my guess would be that we’ll continue to see strong price growth in May. I mentioned last month that the Condo market hasn’t been seeing as much love as the Freehold market, but I’ve started to see signs of this competition bleeding into the Condo market as we get deeper into the spring without any hint of new inventory coming.

As always if you have more specific questions, need advice, or want to talk about what I’m seeing out there, get in touch. I’m always happy to talk shop!